Inventory is a central economic indicator that indicates the quantity of goods, raw materials, semi-finished products and finished products in a company's warehouse at a specific point in time. Optimum warehousing ensures that sufficient stocks are available to ensure availability without unnecessarily tying up a large amount of capital.

Inventory is the entirety of all goods and materials that a company has in stock at a specific reporting date. In the balance sheet, inventory is shown as part of current assets and is part of inventory.

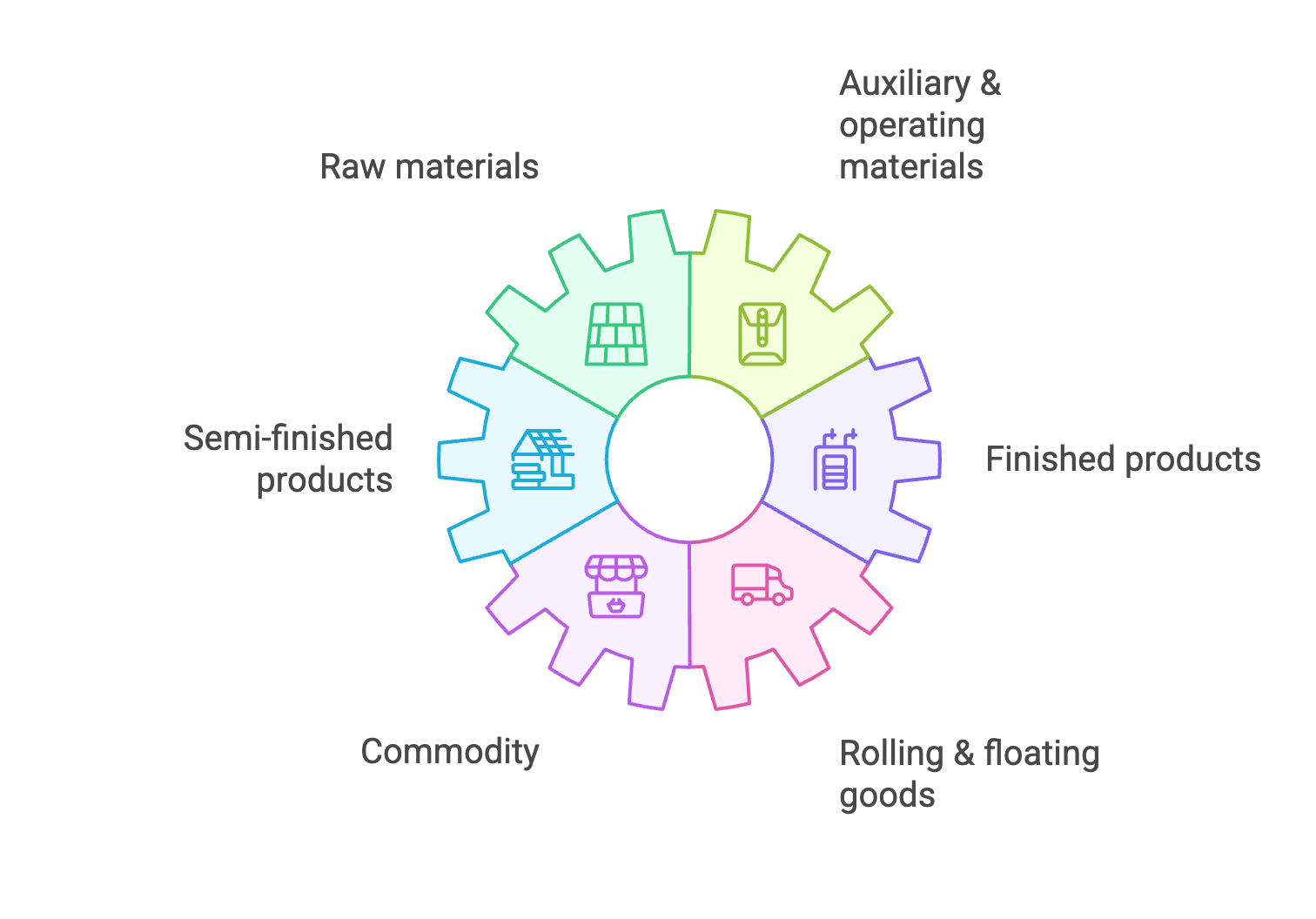

From a business perspective, there are several categories:

Inventory represents fixed capital that is not available for other entrepreneurial purposes. At the same time, sufficient stocks are required to ensure readiness for delivery and to cushion fluctuations in demand or delivery delays.

The basic formula for calculating average inventory is:

Average inventory = (starting inventory + ending inventory)/2

This simple formula is suitable for calculation over a period, such as a quarter or a fiscal year. For a more accurate calculation of fluctuating stocks, a monthly average can also be calculated.

If there are significant fluctuations within the period, this formula is recommended:

Average inventory = (inventory month 1 + inventory month 2 +... + inventory month 12)/12

This method provides more precise values because it takes account of arrivals and departures over the entire period.

Inventory turnover rate: Shows how often the inventory is completely turned over within a period.

Formula: use of goods/average inventory

Average storage period: Indicates how long goods remain in the warehouse on average.

Formula: (Average inventory × 360 days)/Use of goods

Capital commitment: Calculates the capital tied up in inventory.

Formula: Average inventory × purchase price

The optimal inventory is not a fixed quantity, but a compromise between various factors. It must be sufficient to:

At the same time, it should not be too high to:

The optimal order quantity helps to efficiently manage inventory. It takes into account order costs, storage costs and demand. Modern warehouse management systems automatically calculate these values and help specialists and managers optimize them.

Inventory plays an important role in accounting. It is recorded as part of current assets on the balance sheet date and reported as part of current assets on the balance sheet. The valuation is usually carried out at purchase or production costs.

A high inventory ties up capital that is not available for other investments or to pay off liabilities. This can affect a company's liquidity. For retail companies in particular, a balance between inventory and financial resources is vitally important.

As an experienced Fulfillment service provider sustains EMIRAT emFulfillment Companies are able to efficiently manage and optimize their inventories. With modern warehouse management systems and years of expertise, we ensure that you find the right balance between security of supply and capital commitment.

Our range of services includes:

By outsourcing your warehouse management to EMIRAT Fulfillment You can concentrate on your core business while we ensure optimal inventories, low capital commitment and high delivery capacity.

A medium-sized online retailer was struggling with high inventories and a corresponding capital commitment. Through an analysis of inventory figures, it was found that the inventory turnover rate was just 4 per year — well below the industry average of 8-10.

measures:

upshot: The inventory turnover rate rose to 7, the capital commitment fell by 35%, and the ability to deliver remained constant at 98%.

A manufacturer of industrial components struggled with the conflict of objectives between cheap bulk orders of raw materials and high storage costs. The average storage period was 90 days.

measures:

upshot: The average storage period fell to 60 days, storage costs were reduced by 25%, while at the same time purchase prices fell by 8% due to better conditions for strategic items.

A sporting goods retailer had to deal with severe seasonal fluctuations. After the season, large remaining stocks regularly remained, which had to be sold at significant discounts.

measures:

upshot: Remaining stocks after the end of the season fell by 60%, depreciation fell by 40%, and readiness to deliver during the peak season improved to 99%.

The terms are often used interchangeably. Inventory specifically refers to the goods physically in the warehouse, while inventory can also include goods that have not yet been delivered but have already been ordered. In the balance sheet, both are summarized under the term inventories.

For effective management, it is recommended to calculate the average inventory on a monthly basis. The legally required inventory must be carried out at least once a year. Modern warehouse management systems enable real-time monitoring on a daily basis.

This is highly industry-dependent. Values of 20-30 are common in the food trade, while 4-6 can be normal in mechanical engineering. In general, a higher inventory turnover rate indicates efficient warehousing, but should not jeopardize the ability to deliver.

Safety inventory depends on several factors: average delivery time, fluctuations in demand, delivery delays and the desired level of service. A simplified formula is: Safety stock = (maximum daily consumption × maximum delivery time) - (average daily consumption × average delivery time).

Inventory ties up capital that is not available for other purposes. Too much inventory can significantly impair liquidity, as money is tied up in goods rather than in available funds. Optimizing inventory therefore directly improves the liquidity situation.

Rolling goods mean goods that have already been ordered and paid for and are still on their way to the company. Floating goods are a specific term for goods that travel by ship. Both are already part of the company economically, but are not yet physically in the warehouse.

Auxiliaries and supplies are part of the inventory and must be recorded in the inventory. They also tie up capital, but are often neglected during optimization. Close monitoring of these positions as well can result in significant savings.

Capital commitment means the value of the goods in the warehouse that cannot be used elsewhere. It is calculated by: Average inventory × purchase price. High capital commitment reduces financial flexibility and causes opportunity costs.

This classic conflict of objectives requires a balanced strategy: Rely on differentiated safety stocks (higher for critical A items, lower for C items), improve demand forecasting, shorten delivery times through better supplier management and use modern IT systems for precise control.

Inventory is the physical recording of all stocks on a reporting date and is required by law. It is used to check book collections, uncover shrinkage and errors and is the basis for accounting. Discrepancies between book and actual inventory must be investigated and corrected.

Inventory is much more than just a key figure in accounting; it is a strategic success factor for companies. Professional inventory management makes it possible to optimally resolve the conflict of objectives between security of supply and capital commitment.

By systematically calculating and analyzing inventory indicators, implementing modern warehouse management systems and continuously optimizing ordering strategies, companies can significantly reduce their inventory costs, improve liquidity and at the same time increase their ability to deliver.

Whether for retail companies, manufacturing companies or online retailers, finding and maintaining the right balance in inventory is an ongoing task that, when implemented consistently, pays off through measurable results in the balance sheet and improved competitiveness.